EN

ID

Important Note: The results provided below reflect the audited consolidated results of PT Harum Energy Tbk. (“the Company”) for the 3- months period ending 30 April 2026 (“1Q 2026”), which include the results of PT Mahakam Sumber Jaya (“MSJ”), PT Layar Lintas Jaya (“LLJ”),

PT Santan Batubara (“SB”), PT Karya Usaha Pertiwi (“KUP”), PT Bumi Karunia Pertiwi (“BKP”), PT Harum Nickel Perkasa (“HNP”), PT Tanito Harum Nickel (“THN”), Nickel International Capital Pte., Ltd. (“NICAP”), PT Harum Nickel Industry (“HNI”), PT Infei Metal Industry (“IMI”), PT Position (“POS”), PT Westrong Metal Industry (“WMI”), and PT Blue Sparking Energy (“BSE”). The report below is prepared by the management and unaudited.

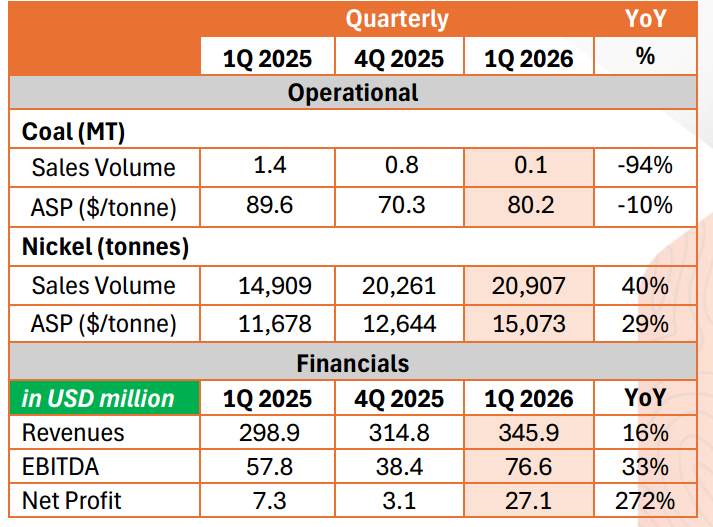

Nickel continues to drive operational growth, with 1Q 2026 sales volume rising 40% YoY to 20,907 tonnes. ASP increased 29% YoY to USD 15,073/tonne, supported by stronger LME pricing and improved product mix. The volume growth was driven by a faster-than-expected ramp-up, reinforcing nickel as the key earnings driver. In terms of contribution, nickel accounted for 97% of revenue and 100% of EBITDA, underscoring its position as the dominant driver of the Company’s performance in 1Q 2026.

Coal performance reflects a sharp downcycle, with sales volume declining 94% YoY and ASP down 10% YoY in 1Q 2026. The minimal output during the quarter was due to delayed government approvals, which constrained production. With approvals now secured, volumes is expected to ramp up from 2Q 2026 onward, and back-end loaded to meet the approved annual RKAB.

Consolidated revenue rose 16% YoY to USD 345.9 million in 1Q 2026, primarily driven by higher nickel sales volume and improved ASP. The revenue mix continues to shift toward nickel, further strengthening the Company’s transition away from coal and supporting a more structurally resilient business profile.

Despite no contribution from the coal business, consolidated EBITDA increased by 33% YoY to USD 76.6 million, reflecting higher nickel sales volume and margin in 1Q 2026. Margins improved for the quarter to 22% from 19% in same period last year due to the nickel segment’s higher ASP and integration.

Consolidated Net Profit surged 272% YoY to USD 27.1 million, rebounding from a low base in 1Q 2025 due to a one off adjustment. The strong growth reflects improved nickel performance and the absence of prior period pressures.

We encourage all readers to read and review the full report attached below for complete details and analysis.

For further information, investors and shareholders can contact: